Student Loan & Financial Aid: the journey through college application student!

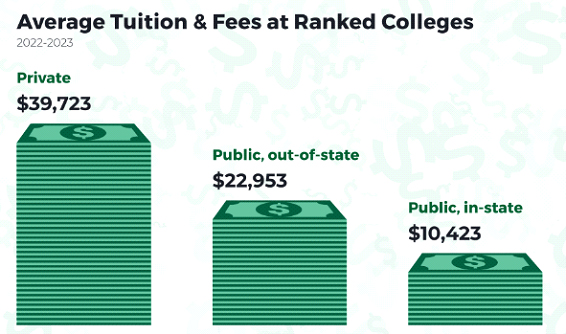

Student loan & Financial Aid are big topics for a student journey, since the early stage in the preparation of the process, students and their parents/relatives need to start the planning paths. The cost of education can be a major barrier, mainly for private schools. The average cost of tuition and fees to attend a ranked public college in state is about 74% less than the average price at a private college, at $10,423 for the 2022-2023 year compared with $39,723, respectively, U.S. News data shows. The average cost for out-of-state students at public colleges comes to $22,953 for the same year, according to USANews/payingforcollege, that cost has climbed 4% over last two years - that includes tuition and fees, on-campus room and board, books, supplies, and other expenses.

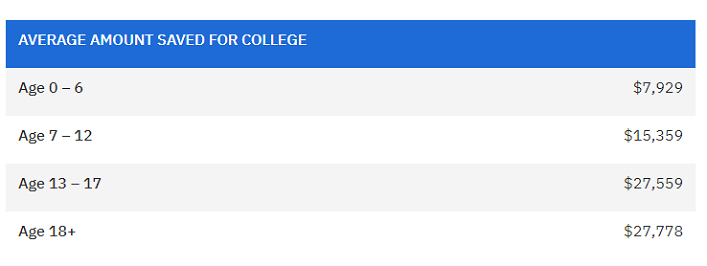

How much should a family need to save for a college?

What are the loan options available for students:

There are several loan options available for college students, that can help students cover the cost of tuitions and their education expenses, some of common loans:

⦁ Federal Direct Subsidized Loans: These loans are available to undergraduate students with demonstrated financial need. The U.S. Department of Education pays the interest on the loan while the student is enrolled in school at least half-time, during the grace period, and during deferment periods. For Federal option the student may filling out the Free Application for Student Aid (⦁ FAFSA) to apply for federal student loans.

⦁ Federal Direct Unsubsidized Loans: loans are available to undergraduate and graduate students regardless of financial need. Unlike subsidized loans, interest accrues on unsubsidized loans while the student is in school.

The main benefit of federal loan is that there are no credits checks, no minimum income requirements, and lower interest rates for undergraduate loans.

⦁ Private Student Loans: These are offered by private lenders, such as banks, credit unions, and online lenders. Private student loans usually have higher interest rates and may require a credit check or a co-signer. The terms and conditions of private loans vary depending on the lender.

Some of private student’s loan options:

⦁ College Ave: ranks as a best overall due to its variety of loan options, in school payment plans (long term repayments as 15years)

⦁ Sallie Mae: for medical school students can borrow up to 100% of total cost attendance

⦁ Earnest: for parents, Earnest has different repayment options for parents, and they can take advantage of a longer-than-usual grace period.

⦁ Sofi: one of the best choices for the best student loan lender for no fees, discounts, lower interest rates and extra benefits for members – but it is required a high credit score.

⦁ Discover: good option for undergraduate loans that covers up to 100% of school expenses, it has competitive rates.

Both federal loans and private loans can help cover tuition, especially in such a costly market. Despite being counterparts, qualifying for a private loan differs considerably compared to a federal loan. Whereas federal options require the FAFSA and the intent to go to school, private student loans require applicants to bring more ($) to the table. In addition to the high interest rates private loan also requires: i) good credit score; ii) need to meet certain meet income requirements; iii) enroll in a qualified education program; iv) cosigner might be required.

It's essential to weigh the long-term impact of taking on student loan debt and consider developing a budget and repayment plan to manage the debt responsibly. The standard repayment plan is the most common, that is by the default repayment plan for federal student loans. It involves fixed monthly payments over a period of 10 years for most loans. It is recommended to contact the loan servicer or lender directly to discuss repayment options, evaluate the potential impact on monthly payments and interest costs, and ensure compliance with the loan terms.

Don’t rule out the college of your dreams just because of the cost. If a college has higher tuition and expenses, students often get more financial aid to help cover the extra cost. Many students face financial barriers that stop them from pursuing a university education, such as low income, family obligations, and high tuition fees. On top of loans options, students should also explore scholarships, grants, and work-study opportunities before turning to loans, as these forms of financial aid do not need to be repaid. Few opportunities for financing education including:

Scholarships: as a form of financial aid that do not need to be repaid. They are typically awarded based on academic achievement, athletic ability, or other special talents. Scholarships can be offered by universities, private organizations, and government agencies. The advantage is that they provide financial support without adding to a student's debt. Nevertheless, scholarships are often limited to specific groups of students, such as those with high academic achievement or specific demographic. Grants: are another form of financial aid that do not need to be repaid. They are typically awarded based on financial need and can be offered by universities, government agencies, and private organizations. The advantage of grants is that they provide financial support without adding to a student's debt. However, grants are often limited in amount and may not cover all of a student's expenses. Work-Study Programs: Work-study programs are a form of financial aid that allow students to work on campus and earn money to help cover their expenses. Work-study programs can be offered by universities and government agencies. The advantage of work-study programs is that they provide students with the opportunity to gain work experience and earn money while they study. However, work-study programs may not provide enough income to cover all of a student's expenses.

In fact, financing education in university is a significant concern for many students and their families. It is recommended to apply for all types of aid: scholarships, grants, work-study opportunities, and review loans available for each of the requirements. Scholarships and grants provide financial support without adding to a student's debt, while loans and work-study programs can provide students with the necessary funds to cover their expenses. It is important for students to carefully consider their options and choose the financing option that best meets their needs and goals. Also, the students will have a grace period before start to payoff their debt after college graduation, so they will be able to plan a payoff process, kicking off after the graduation and inserted in a workplace